Introduction

Managing credit and debt is a crucial aspect of running a successful business. Effective credit management helps businesses preserve a healthy cash flow, reduce bad debts, and promote financial stability. Credit management is a complex process that involves several steps, from assessing a customer's creditworthiness to collecting overdue payments and taking legal action when required. In this article, we will explore the credit management process in detail, discussing the key steps involved and offering practical tips for improving your credit management practices.

What is credit management?

Credit management refers to the process a business uses to extend credit to customers for the purchase of goods and/or services. It involves overseeing the credit extended to customers and ensuring the timely payment of invoices.

The effective management of credit involves a range of activities, including credit checks to assess the creditworthiness of customers, setting credit limits, and monitoring payment history. It also involves establishing policies and procedures for debt collection, negotiating payment plans with delinquent customers, and taking legal action when necessary.

Credit management is an important function for businesses and financial institutions, as it helps them manage their financial risks and maintain a stable financial position.

What are the steps in the credit management process flow?

The credit management process flow typically involves a series of steps that are intended to help businesses manage their credit and debt in a responsible and effective manner. Here are some of the key steps in the process flow:

1. Credit application: The credit management process begins with the credit application process. A credit application for a business typically includes a range of information about the company and its owners, as well as financial information that is used to assess the company's creditworthiness.

Some of the key elements that may be included in a credit application for a business include:

- Basic information about the company, such as its legal name, business type, address, and contact information. It may also include information about the company's products or services, target market, and industry.

- In many cases, the credit application will require information about the company's owners, including their names, addresses, and contact information. This information is used to verify the identity of the owners and assess their creditworthiness.

- The financial information section includes information about the company's revenue, expenses, and assets, as well as its debt and credit history. This information is used to assess the company's financial health and determine its creditworthiness.

- The credit application may also require the company to provide references from other businesses or vendors that it has worked with in the past. These references can be used to verify the company's credit history and assess its reputation in the industry.

- Some credit applications may also require the company to provide references from its bank or other financial institutions that it works with. These references can be used to verify the company's financial stability and assess its ability to pay its debts on time.

2. Credit analysis: Once a credit application is received, the next step is to perform a thorough credit analysis. This involves reviewing the customer's credit history, income, and other financial information to determine their ability to pay. Based on this analysis, the credit manager approves or denies the credit application.

3. Credit monitoring: Once a credit application is approved, the credit manager needs to monitor the customer's credit usage and payment history. This involves tracking the customer's payments, sending out reminders for overdue payments, and following up with the customer if necessary.

4. Debt collection: If a customer fails to make payments on time, the credit manager may need to initiate debt collection activities. This can involve sending out collection letters (dunning letters), making phone calls, and negotiating payment plans with the customer.

5. Legal action: In some cases, the credit manager will need to initiate legal action to recover the debt. This can involve filing a lawsuit, obtaining a judgment against the customer, and garnishing bank accounts.

6. Reporting: Throughout the credit management process, the credit manager must keep accurate records of all credit transactions and debt collection activities. This information is used to generate reports and analyze the effectiveness of the credit management process.

By following these credit management process steps and implementing sound credit management policies and procedures, businesses can improve their financial stability and reduce their exposure to credit risk.

Featured Resource: Finance Leader’s Guide to Mastering AR

Ways to improve your credit management process

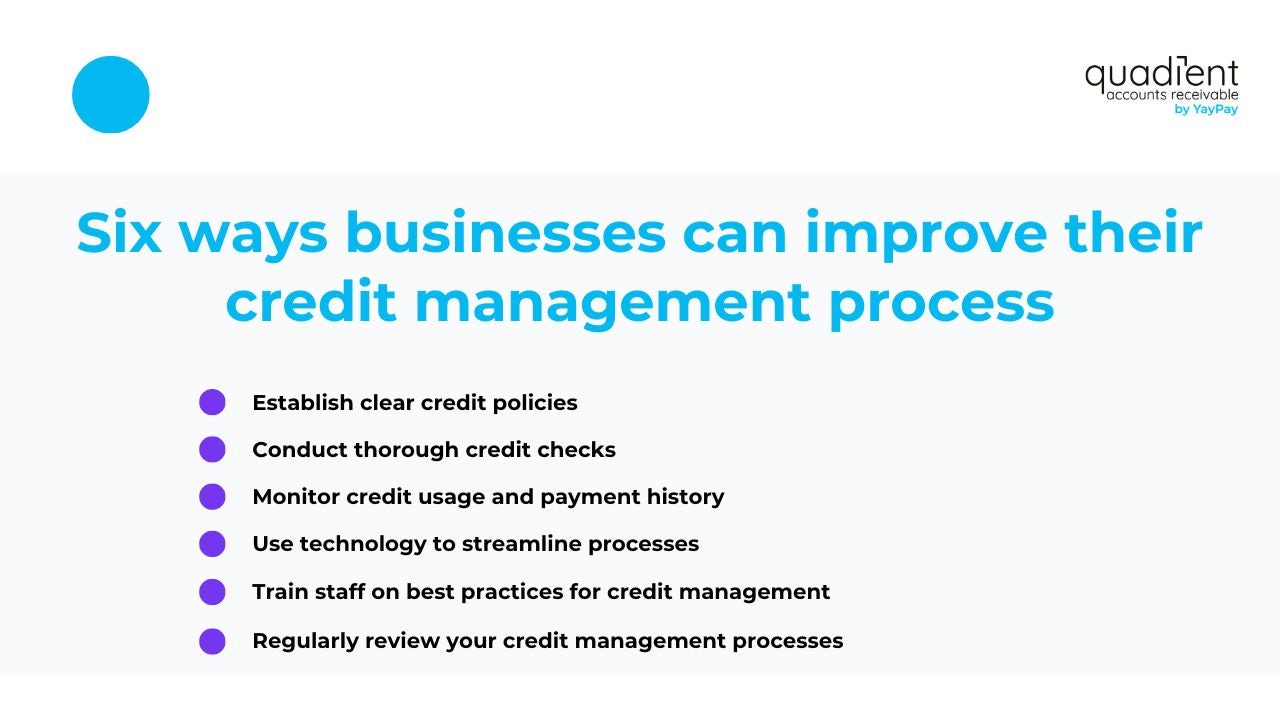

Here are six ways that businesses can improve their credit management process:

- Establish clear credit policies: One of the most important steps in improving credit management is to establish clear policies and procedures for extending credit. This includes setting credit limits, establishing payment terms, and determining the consequences of late or missed payments. By establishing clear credit policies, businesses can ensure that customers understand their responsibilities and reduce the risk of payment disputes.

- Conduct thorough credit checks: It’s essential to conduct a thorough credit check before extending credit to a customer. This involves reviewing the customer's credit history, income, and other financial information to determine their ability to pay. By conducting thorough credit checks, businesses can reduce the risk of bad debts and minimize the need for debt collection activities.

- Monitor credit usage and payment history: Once credit has been extended, it is important to monitor the customer's credit usage and payment history. This involves tracking payments, sending reminders for overdue payments, and following up with customers if required. Monitoring credit usage and payment history can help businesses identify potential payment issues early on and take proactive steps to address them.

- Use technology to streamline processes: There are a variety of software solutions available that can help businesses streamline their credit management processes. This includes tools for automating credit checks, tracking payment history, and sending out payment reminders. By using technology to streamline processes, businesses can save time and reduce the risk of errors.

- Train staff on best practices for credit management: Businesses should invest in training their employees on credit management best practices. This includes educating employees on the importance of credit management, providing training on credit policies and procedures, and offering guidance on how to handle payment disputes and debt collection activities. This ensures that everyone is working together to improve the credit management process and minimize bad debts.

- Regularly review your credit management processes: Businesses should continuously monitor and evaluate their credit management processes to identify areas that need improvement and to adjust policies and procedures accordingly. A proactive approach can help prevent potential credit risks and ensure that the company's financial stability is maintained.

Conclusion

Credit management is crucial for a business's financial stability, preserving cash flow, and reducing bad debts. The credit management process involves several steps, such as credit application, credit analysis, credit monitoring, debt collection, legal action, and reporting. Businesses can improve their credit management practices by establishing clear policies, conducting thorough credit checks, monitoring credit usage and payment history, using technology to streamline processes, and training staff on best practices for credit management. Through these efforts, businesses can reduce their exposure to credit risk and improve their overall financial position.